Framing note — This article draws on the recent work of Henry Maxey (formerly a wealth manager in Zurich), whose two papers, one theoretical and one empirical, formalize what the author calls the "rentier asset black hole theory". His conclusions converge with a broader body of literature ranging from Adam Smith to David Ricardo, through Minsky and contemporary post-Keynesian theory. The aim of this article is not to add another layer of alarmism, but to draw the regulatory and institutional consequences with the rigour they deserve.

I. The Diagnosis: When Capital Stops Creating and Starts Accumulating

1.1 The Fundamental Distinction That the Mainstream Has Forgotten

There is a conceptual confusion at the heart of contemporary macroeconomics, and it is far from trivial: the conflation of productive capital with rentier assets. This distinction, which was central to classical economics — Adam Smith already drew it, Ricardo built an entire theory of differential rent upon it — has gradually disappeared from dominant models over the course of the twentieth century, as neoclassical theory unified the factors of production under a single analytical category.

In a normal productive economy, a price signal triggers a self-regulating chain of reactions: the return on an asset rises, the profit motive induces firms to increase supply, the additional supply normalises the price, and returns stabilise. General equilibrium works. Capital circulates, transforms, creates. This is the model that most theoretical frameworks implicitly assume.

But this model breaks down the moment an asset cannot respond to a capital inflow by expanding its supply. Land is the perfect archetype. Land cannot be manufactured. When capital flows into it, only the price rises. Supply does not adjust. The self-regulating equilibrium never kicks in.

1.2 The Three Conditions of the Trap

For an asset to become what Maxey calls a "rentier black hole", three conditions must be simultaneously present:

Condition 1, Structural inelasticity of supply. The supply of the asset cannot increase directly in response to a capital inflow. Land, certain urban locations, certain scarce rights satisfy this condition. Capital flows in; supply does not move; the price rises mechanically.

Condition 2, Use as bank collateral. Banks recognise in this asset a stable guarantee value. Better still: when its value rises, their lending capacity expands, because their collateral base grows. Debt feeds the rise, which feeds the debt. The loop is closed.

Condition 3, Preferential tax treatment. The tax systems of most developed economies grant these assets advantages that productive assets do not enjoy: exemption of the primary residence from capital gains tax, moderate taxation of rental income, absence of a recurring tax on market value. This preferential treatment increases the risk-adjusted return of the rentier asset relative to any productive alternative.

When these three conditions coexist, no equilibrium assumption holds any longer. Even under the assumptions of market efficiency, even with perfectly rational households optimising their allocations according to Markowitz, the system drifts towards total accretion. All available capital flows toward the rentier asset. There is no stable intermediate equilibrium. There are only two terminal states: the exhaustion of the productive economy (rents exceed what households can pay) or an exogenous shock that fractures the edifice.

1.3 The Phenomenology of the Black Hole: Five Symptoms Predicted by the Model

What makes this model intellectually compelling is that it formally predicts five observable symptoms — not after the fact to fit the data, but as necessary consequences of the theoretical structure:

Symptom 1, The growing gap between real wages and productivity. Capital that should have been invested in machinery, software, R&D, and training has been sucked into real estate. Effective productivity stagnates. Real wages follow. The United Kingdom displays the largest such gap in the developed world. This is not a coincidence: it is the prediction.

Symptom 2, The contraction of the wage share in value added. The rent captured by holders of land and property assets grows structurally at the expense of labour income. This is a silent and continuous redistribution, invisible in GDP statistics because imputed rent appears there as output.

Symptom 3, The explosion of household price-to-income ratios. The ratio between the median house price and the median annual household income has risen, in most affected economies, from 3–4x in the 1980s to 8–12x today in major cities. This ratio is no longer cyclical: it is structurally increasing.

Symptom 4, The rise of wealth inequality. The rentier land economy is fundamentally inegalitarian: it transfers wealth from those without assets to those who have them, automatically and permanently, regardless of merit, effort or productivity.

Symptom 5, The slow and continuous decline of the productive economy. Industrial disintermediation, underinvestment in R&D, atrophy of fixed capital: the productive economy contracts from a relative lack of capital, to the benefit of a hypertrophied financial and property sector.

These five symptoms are present in the United Kingdom, Australia, Canada and New Zealand to varying degrees, and are correlated precisely with the intensity with which each country satisfies the three conditions of the model.

II. Proof by Exception: What Germany and France Teach Us

2.1 Germany: Breaking the Collateral Loop

Germany is the first remarkable exception. It partially satisfies Condition 1 (land supply is inelastic, as everywhere), but it breaks Condition 2 in an institutional manner. The German mortgage system, the Pfandbrief, prohibits banks from valuing residential property used as collateral at its current market value. The valuation must be based on a long-term value (Beleihungswert), which is structurally lower than the market value during periods of rising prices.

Consequence: when property prices rise, banks' capacity to lend does not increase proportionally. The positive feedback loop is broken. Capital cannot flood into the asset with the same amplified leverage effect. The accretion mechanism is neutralised.

2.2 France: Breaking the Return Loop

France takes a different route. It breaks Condition 3 through taxation. The IFI (Impôt sur la Fortune Immobilière — Real Estate Wealth Tax) levies a charge on property holdings above a certain threshold, with a marginal rate reaching 1.5% of the market value annually. Capital gains on secondary residences are taxed significantly. The taxation of rental income, while imperfect, remains substantial.

These mechanisms reduce the risk-adjusted return on property to the point where its superiority over productive assets is no longer so overwhelming. Capital does not flee massively into real estate, because the return differential is partially absorbed by taxation.

These two exceptions are not accidental. They result from deliberate institutional choices, built up over decades. They prove that the mechanism is not a natural inevitability: it is the product of rules that societies give themselves, and that they can modify.

III. Structural Market Failure: Why the Invisible Hand Cannot Correct This Alone

3.1 A Textbook Case of Endogenous Market Failure

The great theoretical lesson of this model is that it generates a structural market failure even under the most favourable conditions for efficiency: perfect markets, perfect information, rational agents. This is not a failure caused by information asymmetries, classic negative externalities, or market power. It is a failure caused by the very structure of the asset and the institutional rules that govern it.

In this framework, the market cannot self-correct. The accretion loop is rational at every individual level: each household, each bank, each investor makes decisions perfectly consistent with their individual interests. It is precisely the coherence of these individual decisions that produces the disastrous collective outcome. This is a problem of systemic coordination, not of individual rationality.

Game theory is illuminating here: we are in a large-scale prisoner's dilemma structure, where the Nash equilibrium (everyone invests in real estate) is suboptimal for the whole, but no isolated agent can unilaterally deviate from it without penalising themselves. External intervention — that is, the State — is the only institution capable of changing the rules of the game to achieve the collective optimum.

3.2 The Illusion of GDP as a Compass

A particularly insidious aspect of this dynamic is that it remains invisible in standard macroeconomic indicators for as long as it progresses. National accounting includes imputed rent in GDP: the value of housing services that owner-occupiers render to themselves, calculated on the basis of market rents. When property prices rise, imputed rent rises, and GDP rises. The growth is statistically real, but it corresponds to no additional production of tangible goods or services.

Public decision-makers are therefore navigating with a biased instrument. Measured growth reassures them at the very moment when the productive economy is contracting. This accounting bias is fundamental: it pushes back the moment when public policy perceives the need to intervene.

3.3 The Event Horizon and the Loss of Information

Beyond a certain accretion threshold, returns on capital are no longer diminishing: they become increasing. The ordinary laws of macroeconomics cease to apply. This is what Maxey calls the "event horizon" of the rentier black hole. Past this threshold, standard forecasting and regulatory models lose their validity. One enters a regime of non-linearity where corrections become exponentially more costly.

The loss of information is the dimension most difficult to grasp politically: we do not know what would have been built, invented, or founded if this capital had not been absorbed. The factories not built appear in no statistics. The companies not founded have no register. The innovations that never happened have no balance sheet. It is a loss that cannot be seen, and that is precisely why it is politically difficult to mobilise around.

IV. The Role of the State: Not an Ideology, but a Structural Necessity

4.1 Rethinking the Normative Framework for Public Intervention

Too often, the debate on the role of the State in the economy is framed as an ideological debate: State versus market, collective versus individual, left versus right. This framing is sterile and, in the present case, misleading. The question posed by the rentier black hole theory is not ideological: it is functional.

If a structural market failure generates an inevitable trajectory of collective impoverishment without external intervention, and if only an institution endowed with legitimate coercive power can change the rules of the game, then the question is not "should the State intervene?" but "how should it intervene, with what instruments, at what scale, and with what governance guarantees?"

This reframing matters. It shifts the debate from the terrain of values to that of institutional engineering — a more operational and less sterile terrain.

4.2 The Levers of Intervention: A Hierarchical Toolkit

Lever 1, Recurrent wealth taxation.

This is the most direct lever for breaking Condition 3. An annual tax on the market value of real estate assets — whether a land value tax (LVT) on the value of land alone, as Henry George proposed in the nineteenth century, or a broader tax of the reinforced IFI type — mechanically reduces the risk-adjusted return of the rentier asset. It narrows the return differential with productive assets. It progressively redirects savings flows.

An LVT has an additional theoretical advantage: it does not tax the improvement made by the owner (construction, renovation), but only the value of the land itself, which is a collective value, a product of accessibility, infrastructure, and surrounding public amenities. Taxing it amounts to capturing for the community what the community has itself created.

Lever 2, Reform of banking collateral regulation.

The German example is replicable. Prudential regulators (in Europe, the ECB and the relevant national authorities within the banking union framework) can require that the value of real estate collateral used in the calculation of capital ratios be based not on the current market value, but on a less volatile long-term valuation. This breaks the feedback loop between rising prices and credit expansion.

This reform does not require primary legislation in most European jurisdictions: it falls within the regulatory powers of banking supervisors. Its impact on accretion dynamics would be significant without being abrupt.

Lever 3, Public land supply policy.

If Condition 1 (supply inelasticity) is partly natural (land cannot be created), it is also partly institutional: land-use restrictions, density rules, and the excessive protection of existing land rents through planning regulations all constitute barriers to entry in the housing supply. An effective regulatory State can, and should, remove these barriers where they do not correspond to genuine negative externalities (biodiversity protection, natural risk prevention), and maintain them where they correspond to legitimate collective interests.

Furthermore, the constitution of public land reserves, the use of public land agencies, and the mobilisation of under-used public land constitute direct supply levers that the State can activate without waiting for the private sector to engage.

Lever 4, Reorientation of public investment toward productive capital.

The share of public investment expenditure (public GFCF) in GDP has tended to decline in developed economies since the 1980s, under the combined effect of austerity policies and the rise of public debt. Yet public investment in fixed capital — infrastructure, education, R&D, the energy transition — plays a role that is the inverse of crowding out by the rentier asset: it attracts private capital into productive activities, increases total factor productivity, and generates positive externalities that the market alone cannot internalise.

Reorienting public investment toward these sectors is both a short-term macroeconomic policy (demand support) and a long-term structural policy (rebuilding the stock of productive capital).

Lever 5, Anticipatory macroprudential governance.

Macroprudential authorities (in France, the HCSF; at the European level, the ESRB) have tools to act in an anticipatory manner on bubble dynamics: loan-to-value ratio limits, countercyclical capital requirements, and sectoral restrictions on mortgage lending volumes. These tools exist. They are under-used relative to their stabilisation potential.

Strengthening the mandate of these authorities — by explicitly giving them the mission of monitoring and correcting feedback loops between asset prices and bank credit — would represent a significant institutional advance without overhauling the existing regulatory framework.

4.3 The Question of Sequencing and Transition Effects

Any regulatory intervention in markets as deep as real estate carries a non-negligible transition risk. A sharp correction in prices, even if desirable in the long run for society as a whole, can trigger banking crises (through collateral depreciation), wealth destruction for indebted households, and short-term demand crises.

Public policy must therefore be designed to act on the trajectory, not on the level. The objective is not to bring prices down rapidly — which would be economically and politically destructive — but to stop their relative growth compared to incomes, to progressively eliminate the comparative advantage of the rentier asset, and to allow the readjustment to take place over a time window of ten to twenty years.

This type of policy requires long-term institutional planning that short electoral cycles make difficult. This is an additional argument for entrusting the management of these instruments to independent institutions — central banks, macroprudential authorities, public land agencies — endowed with stable, multi-year mandates.

V. Prospective Implications: The Cost of Inaction

5.1 The Baseline Scenario Without Correction

If no lever is activated, the model predicts a continuation of the current trajectory. The wage share will continue to decline. The productivity gap will widen. Price-to-income ratios will continue to grow until one of the two terminal conditions is reached: the insolvency of the productive economy (households can no longer pay their rents or mortgage repayments from their incomes) or an exogenous shock (deep recession, financial crisis, pandemic) that fractures prices.

This terminal scenario is not far off in certain geographies. Cities like Sydney, Auckland, Toronto or London are approaching price-to-income ratios that make home ownership mathematically impossible for the majority of working households. This is no longer a social tension: it is a breakdown of the intergenerational social contract.

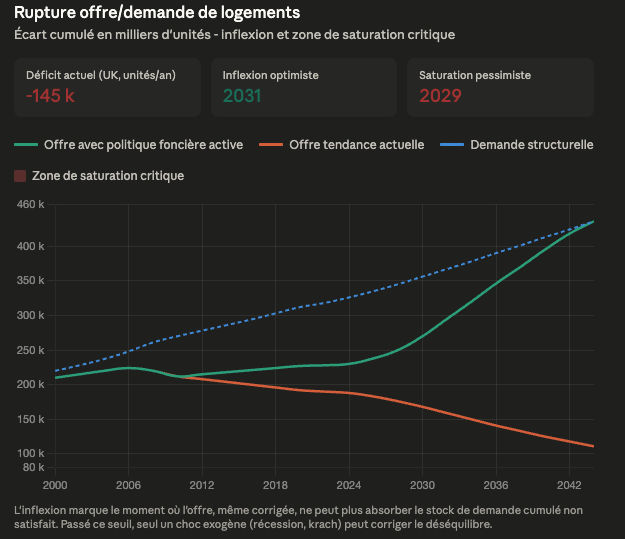

On public investment, the divergence is not linear — it accelerates after 2030 in the pessimistic scenario because contracting public investment speeds up the flight of capital toward rentier assets, which in turn depresses available tax revenues. This is a self-sustaining underfunding spiral.

On the cost-to-income ratio, the 9x threshold is not arbitrary: it is the point at which a median first-time buyer, with a standard deposit, exceeds a 40% debt-to-income ratio on their disposable income — what prudential standards consider the limit of individual affordability. This threshold has already been crossed in UK, Australian and Canadian cities. The question is no longer how to avoid crossing it, but whether we pull back or continue to make it worse.

On the supply/demand breakdown, the red zone (2024–2034) represents the critical window: this is where the gap between the two trajectories opens up irreversibly. The optimistic scenario does not eliminate the deficit immediately — it reverses the slope. The pessimistic scenario, meanwhile, reaches a point of no return around 2029, where even a sharp price correction would no longer be sufficient to rebalance the market without massive destruction of bank capital.

5.2 The Cost of Inaction in Terms of Human Capital and Innovation

The most difficult loss to quantify is that of intellectual and entrepreneurial capital. When an entire generation devotes a growing share of its income and energy to accessing housing, it devotes less capital, time and attention to entrepreneurial risk-taking, extended education, and geographical mobility toward high-innovation areas. The rentier land economy is an economy of sedentariness and conservation, the antithesis of the economy of innovation and disruption.

Empirical analyses of residential mobility show that high-price, low-turnover housing markets significantly reduce worker mobility, including toward more productive jobs. The "agglomeration" dynamic that accounts for a major share of productivity growth in cities is itself impeded by the cost of housing.

5.3 The Political Window of Opportunity

In democratic economies, there exists a moment when the social suffering linked to a systemic failure becomes sufficiently visible and widespread to open a political window for intervention. The data suggest that several of the affected countries are approaching this moment: the 25–40 age cohort, statistically excluded from home ownership in major cities, is beginning to carry significant electoral weight.

This window will not remain open indefinitely. Systemic crises, if not managed during their development phase, tend to resolve themselves brutally and without direction — either through financial collapse or political radicalisation. Both outcomes are more costly than preventive regulation.

VI. Conclusion: The State as a Condition of Possibility for the Market

It must be stated clearly, because it is a proposition that the liberal orthodoxy of the past forty years has systematically obscured: markets are not natural phenomena. They are institutional constructions. They function well or badly depending on the rules that frame them, the property rights they presuppose, the public guarantees from which they benefit, and the externalities they generate.

The housing market, as it is organised in most Anglo-Saxon economies, is not a market that fails by accident. It fails by design: its tax rules, its banking regulation and its planning restrictions have been shaped by decades of lobbying by existing asset-holders, who had a direct interest in the perpetuation of rent.

Correcting this failure does not mean "more State" in the ideological sense of the term. It means correcting poorly designed rules with better-designed ones. It means aligning individual incentives with collective interests — which is precisely the primary mission of a well-calibrated institutional architecture.

The tools exist. The working examples exist — Germany and France demonstrate this. The theoretical knowledge is available, even if it has been ignored for too long. What is lacking is the political will to deploy these tools with the necessary coherence and persistence.

The stakes are not modest. If the model holds — and the empirical data converge in that direction — several decades of lost productive capital, a generation deprived of social mobility, and a structural decline of the West are directly attributable to this collective forgetting of a distinction that the founding fathers of political economy had stated clearly.

The moment for correction is now time-constrained. The longer we wait, the deeper the lock-in effects become, the more costly the correction will be, and the more likely unmanaged outcomes become.

This is not a question of economic philosophy. It is a question of urgent institutional engineering.

Primary sources: Henry Maxey, "The Rentier Asset Black Hole Theory" (working papers, 2024–2025); Adam Smith, Wealth of Nations (1776); David Ricardo, Principles of Political Economy (1817); Minsky, H.P., Stabilizing an Unstable Economy (1986); OECD, Housing and the Economy (2021); ECB, Financial Stability Review (2023).